- €84 million: what Dutch return points were paid in 2024 for their role in the deposit scheme. The only part of the system that pays retailers for their role.

- $393 billion: where secondhand apparel is heading by 2030, growing twice as fast as apparel retail overall (US-led data). Where the object holds value, brands already run identified take-back.

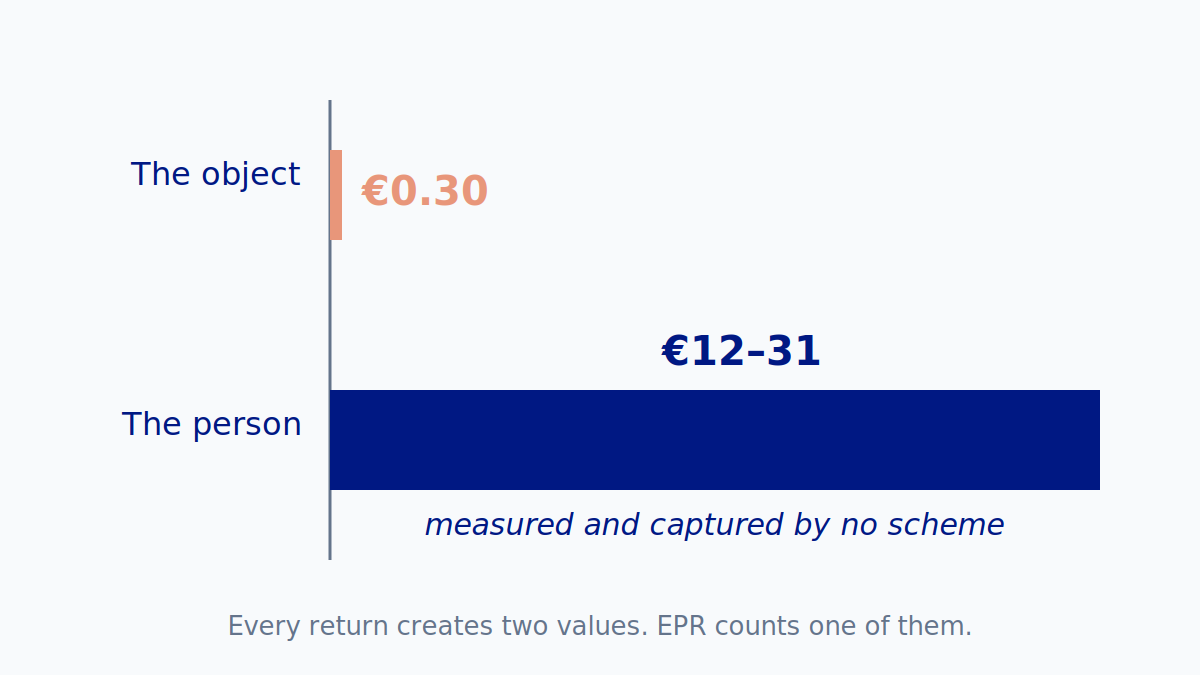

- €1–3: the evidenced cost of a verified customer email with product data, captured at the point of return, against roughly €25 for a paid-social lead. The fee system does not capture this value.

This part is about who pays for everything, and what they should be asking for.

Add up what brands and retailers are paying into the system:

- an eco-contribution on every item placed on the market, rising year on year

- floor space for the collection point, mandated take-back for electronics, batteries and vapes, handling and staff

Then list what comes back:

- legal permission to sell

- a logo for the label

- an annual report measured in tonnes

The fee funds the campaign; the campaign moves a percentage of customers, who walk into stores or communal collection locations carrying a product, hoping the right thing happens.

Nobody knows who came, which products were left, or what happened next. What is worse? If the fees prove to be insufficient - the reaction is to go back to the brands and retailers and ask for more money.

There are examples where retailers are compensated

Deposit systems pay retailers for their part: a handling fee of a few cents per container returned. In the Netherlands, return points received 84 million euros in compensation in 2024, funded by the scheme. Everywhere else, retailers are required to host take-back and are not paid for it.

So there is a precedent: the best-performing scheme type pays retailers for their participation. The customer value that retail brings to every return is still not measured or paid for anywhere.

Not all products are worthless - resale and repair create measurable value

Look at what brands and retailers do when a used product still holds value.

- Decathlon runs buyback

- IKEA buys back furniture

- Apple and Samsung run trade-in at scale

- Patagonia built a brand on repair

Secondhand apparel is heading for 393 billion dollars by 2030, growing twice as fast as apparel retail overall (US-led data). And legislation is pushing the same way: by the end of this month, every EU member state must have the right to repair written into national law, and France’s textile scheme already routes 12 of every 100 fee euros into repair bonuses.

Every one of those programmes is a take-back where the customer is identified by default, the product is identified by default, because it is being priced, and the return is engineered to produce the next purchase. Nobody had to legislate that design. Marketing gets behind it because the value was easy to measure and worth capturing.

We covered this in part one: identified take-back follows the object’s value. The same customer walking through the same door with the same brand’s product is a named trade-in customer while the item holds value, but the moment the item is worthless, we direct it to a channel where everything, and everyone, becomes anonymous. Retail treats those as two different worlds. The customer does not.

The same approach works when the product is worthless

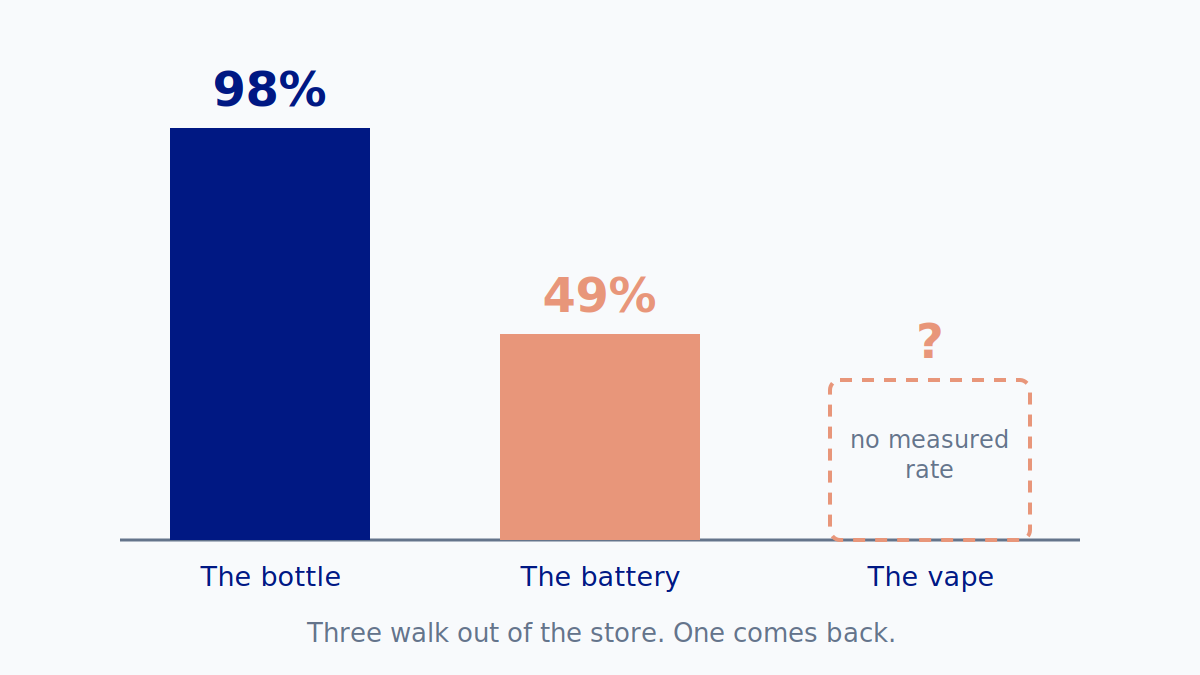

The trade-in desk proves the design. The question is whether it transfers to the box, where the object is worth nothing. It does, and it has been measured: in the published Dutch footwear pilot, five stores took back more than 750 pairs from more than 600 identified customers, with identification at the point of return around 90 per cent.

The cost of a verified customer email with product-level data attached, captured at the return: one to three euros. The same marketing departments pay around 25 euros for a paid-social lead, and 42 to 69 euros to acquire a customer outright.

The customers are walking into stores already

For brands and retailers, the first move is already in your control. The store is yours, the box is in it, the customer is yours to ask, and the consent is theirs to give. The pilot above was retailers doing precisely this, at end of life, without waiting for any scheme to change.

The bigger question is for the schemes. It is not asking schemes to collect customer data, it is asking the schemes to measure it. EPR fees already pay to create this activity: the campaigns move people, the collection boxes receive the products.

Unmeasured, that spending remains a reported cost, and increased activity is reported as tonnage. Brands and retailers see the fees collected as a receipt.

If a brand or retailer can collect and report detailed participation data, their view of the fee changes immediately. This matters because fees are rising in every stream in this series, and payers will resist every increase they cannot see an outcome for.

Product passports change less than people hope

Product identity is arriving by law: under the EU’s ecodesign rules, garments are expected to carry a digital product passport around 2028 to 2029. It is tempting to treat that as the missing piece. It is not, for reasons I set out in The compliance gap nobody owns: almost nothing on the market today carries a passport, almost nothing sold between now and the deadlines will either, and the stock arriving at take-back points for years to come is exactly the stock the passport was never going to describe.

And a passport only helps if someone scans it. Unless retailers and brands build return systems that are easy to use and give the customer a reason to care, the passports will not be scanned. The identification technology is not the constraint. The customer’s motivation is.

Count the customer

This series has made one argument, in three parts:

- Part one. Every return creates two values: the object and the customer. The system counts the object, and for most products the object is worth nothing.

- Part two. The machinery to capture both is not hypothetical. Deposit systems identify the product, confirm the person and pay the incentive, at national scale, inside retail stores.

- Part three. Brands and retailers can capture the customer today, in their own stores, with consent, for less than any channel they currently pay for. The schemes only need to measure what their fees already create.

Count the customer alongside the object, and the economics of every scheme in this series change. A scheme that can show the participation its spending creates is selling what it actually delivers. A scheme that cannot is selling itself short, in front of exactly the people it is asking for support.

Neither move needs to wait for the other.

Full evidence base, with sources, on our research pages. Part one · Part two.